- Home

- Retirement

- Happy Retirement

For Gen X, delaying retirement can be an opportunity to pilot-test your second act, plan for your inheritance and structure trusts for your kids.

By

Jacob Schroeder

published

28 February 2026

in Features

By

Jacob Schroeder

published

28 February 2026

in Features

When you purchase through links on our site, we may earn an affiliate commission. Here’s how it works.

- Copy link

- X

Profit and prosper with the best of Kiplinger's advice on investing, taxes, retirement, personal finance and much more. Delivered daily. Enter your email in the box and click Sign Me Up.

Contact me with news and offers from other Future brands Receive email from us on behalf of our trusted partners or sponsors By submitting your information you agree to the Terms & Conditions and Privacy Policy and are aged 16 or over.You are now subscribed

Your newsletter sign-up was successful

Want to add more newsletters?

Delivered daily

Kiplinger Today

Profit and prosper with the best of Kiplinger's advice on investing, taxes, retirement, personal finance and much more delivered daily. Smart money moves start here.

Signup +

Sent five days a week

Kiplinger A Step Ahead

Get practical help to make better financial decisions in your everyday life, from spending to savings on top deals.

Signup +

Delivered daily

Kiplinger Closing Bell

Get today's biggest financial and investing headlines delivered to your inbox every day the U.S. stock market is open.

Signup +

Sent twice a week

Kiplinger Adviser Intel

Financial pros across the country share best practices and fresh tactics to preserve and grow your wealth.

Signup +

Delivered weekly

Kiplinger Tax Tips

Trim your federal and state tax bills with practical tax-planning and tax-cutting strategies.

Signup +

Sent twice a week

Kiplinger Retirement Tips

Your twice-a-week guide to planning and enjoying a financially secure and richly rewarding retirement

Signup +

Sent bimonthly.

Kiplinger Adviser Angle

Insights for advisers, wealth managers and other financial professionals.

Signup +

Sent twice a week

Kiplinger Investing Weekly

Your twice-a-week roundup of promising stocks, funds, companies and industries you should consider, ones you should avoid, and why.

Signup +

Sent weekly for six weeks

Kiplinger Invest for Retirement

Your step-by-step six-part series on how to invest for retirement, from devising a successful strategy to exactly which investments to choose.

Signup + An account already exists for this email address, please log in. Subscribe to our newsletter

For decades, retirement has been marketed as a long-awaited escape from work, stress and obligation. But for many Americans, that finish line is moving farther away. In some cases, that's a conscious choice to set aside extra savings or stay at a fulfilling job. Others may feel stuck in their career.

If you're still working past your chosen retirement age, there are several ways to reframe the experience and build joy and purpose into your work life.

Consider Gen Xers now approaching their 50s and 60s. Some expected they'd be retired by now. Instead, they’re still working — not because they failed, but because life intervened. Their generation has faced challenges such as the Great Recession and must now deal with rising health care costs and longer lifespans.

From just $107.88 $24.99 for Kiplinger Personal Finance

Become a smarter, better informed investor. Subscribe from just $107.88 $24.99, plus get up to 4 Special Issues

CLICK FOR FREE ISSUE

Sign up for Kiplinger’s Free Newsletters

Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more - straight to your e-mail.

Profit and prosper with the best of expert advice - straight to your e-mail.

Sign upAccording to BlackRock’s annual retirement report, just 54% of Gen X respondents say they are on track to meet their retirement goals — the lowest confidence level of any generation surveyed.

And the strain isn’t just financial. It’s emotional. Identity-shifting. That level of change can feel demoralizing.

"I talk with people every day who feel like they've played by the rules, worked hard their entire lives, lost their jobs, and are frustrated because they have to work but can't find a new job," says Colleen Paulson, founder of Ageless Careers, a career coach who works with older professionals navigating late-career transitions.

For a growing share of workers, the question isn’t "When can I retire?" but "How do I stay motivated and fulfilled if I have to keep working?"

The good news: Delayed retirement doesn’t have to feel like failure. For some, it becomes a chance to redesign work, purpose and lifestyle, rather than simply waiting for an escape.

Why the retirement finish line keeps moving — and how working a few more years can help

More than one in three U.S. adults (35%) say they have already delayed or expect to delay retirement, according to a recent New York Life survey. The top reasons: insufficient savings (51%), inflation (46%) and economic uncertainty (32%).

For Gen X, there’s often another pressure point: caregiving.

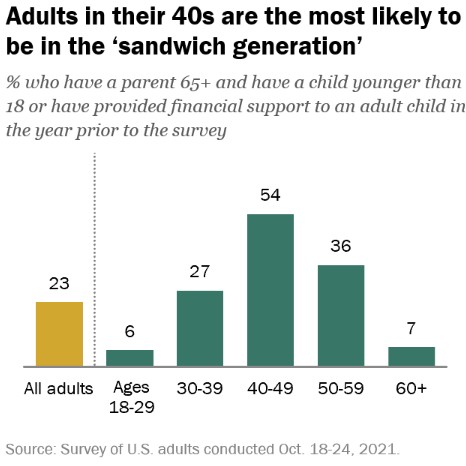

About 23% of U.S. adults are now part of the so-called "sandwich generation," supporting both aging parents and children, according to Pew Research. Among Americans in their 40s, more than half are balancing care for a parent 65 or older while still supporting kids or adult children — a generational squeeze that makes early retirement harder to sustain.

Patrick Huey, owner and principal adviser of Victory Independent Planning, sees the emotional toll firsthand.

"Many of the Gen X clients I work with are discovering that the ‘traditional’ script — retire in your early 60s and coast — isn’t realistic on their original timetable. Emotionally, I hear the same words over and over: Burnout, resentment, fear."

One potential upside, he says, is that delaying retirement by even a few years can help buy breathing room.

"A big reason retiring at age 65 is safer is simple but underappreciated: health care is a massive line item, and in the U.S., Medicare eligibility at 65 is a financial pivot point. Bridging several years of private insurance can cost tens of thousands per year for a couple."

In that sense, continuing to earn income from 62, the average retirement age, to 65, even part-time, can reduce portfolio withdrawals, preserve employer health coverage and ease long-term financial strain.

Redesign your work, not just your exit

Nearly half of Gen X (48%) say they plan to continue working during retirement, or already are, according to Northwestern Mutual. Among Boomers, fewer than one in three say the same. Most Gen Xers working or planning to work in retirement say they will continue to do so out of necessity.

If retirement has to wait, Paulson encourages older workers to shift their mindset from frustration to a sense of control.

"For me, it's about focusing on what you can control. For those of us who have raised our children, this can be a time of great freedom, where we can live where we want to live and work in a way that works for us," she says.

Rather than clinging to traditional corporate paths, she sees many late-career professionals intentionally reinventing their work, noting: "I have had numerous clients who have decided to step out of Corporate America into nonprofit work — they have purposely taken pay cuts because they want to work for organizations that they believe in."

Huey frames the shift less as a postponement of retirement and more as a redesign of it. "The breakthrough usually comes when we stop treating ‘retire/don’t retire’ as a light switch and start designing a phased second chapter instead," he says.

In practice, that might mean shifting to part-time work, consulting, internal role changes or building a portfolio career — preserving income and benefits while reducing stress and reclaiming autonomy.

Build your retirement life before retirement

One potential emotional challenge of delayed retirement is putting life on hold. That is, postponing joy, hobbies, friendships or travel until some future finish line.

Huey urges clients to resist that mindset: "Build non-work identity and community before you leave. Start some of the ‘retirement life’ now — hobbies, volunteering, time with friends — so you’re not putting your whole life on hold until a specific age."

Paulson echoes the value of experimenting before retirement officially begins. "Volunteer work is a great way to contribute to your community and sometimes leads to paid opportunities. Take the time to think about what would mean the most for you — and then plan accordingly," she says.

In fact, research has linked volunteering in older adulthood to better physical health, improved mental well-being, a stronger sense of purpose and deeper social connection.

Seen this way, delayed retirement doesn’t have to feel like a waiting room. It can become a chance to start living pieces of the life you want now and developing habits that will keep you happy in retirement, instead of deferring them to an uncertain someday.

Sequence goals instead of canceling them

One of the healthiest mindset shifts is replacing "I can’t" with "not yet."

"Sequence goals instead of canceling them," Huey advises. "Delayed retirement often means rescheduling, not giving up: one big trip every other year instead of every year, downsizing a bit earlier to cut fixed costs, being more selective about financial help to adult children until Medicare and Social Security are in place."

He describes a Gen X couple who originally planned to retire at 60:

"A Gen X executive couple came in convinced they had to quit at 60 ‘for sanity.’ The math argued for 65… She moved to a lower-stress internal role; he shifted into project-based consulting. They preserved coverage, eased daily stress, and the later date became tolerable because 60–65 looked nothing like 40–55."

Focus on flexibility over perfection

Sean Pearson, CFP and financial advisor at Ameriprise, reminds clients that comparison is often the thief of joy.

"Comparing our retirement, and all the choices that lead up to retirement, to that of our neighbor or anyone else is far more likely to cause financial stress than help us towards our goal," he says.

He adds, "Most of the stress about retirement comes from our own internally imposed timelines."

But in reality, retirement timing is often shaped less by spreadsheets than by life events. "Health issues, job loss, divorce or relocating to support a spouse’s career are also reasons — often outside of our control — that can influence major life decisions," he says.

In his experience, the people who fare best over time aren’t those who follow a perfect plan but those who preserve room to adapt. "Sometimes the people who end up in the best situation in the long run had the flexibility to overcome life’s financial, personal and health challenges that happen along the way."

That flexibility might include diversified savings, multiple income streams or simply the willingness to adjust expectations without self-blame.

As the author and poet Maya Angelou eloquently put it: "You may not control all the events that happen to you, but you can decide not to be reduced by them."

Read More

- I Thought My Retirement Was Set — Until I Answered These 3 Questions

- 8 Boring Habits That Will Make You Rich in Retirement

- Average Net Worth by Age: How Do You Measure Up?

- Baby Boomers vs Gen X: How They Approach Retirement Differently

Jacob SchroederSocial Links NavigationContributor

Jacob SchroederSocial Links NavigationContributorJacob Schroeder is a financial writer covering topics related to personal finance and retirement. Over the course of a decade in the financial services industry, he has written materials to educate people on saving, investing and life in retirement. With the love of telling a good story, his work has appeared in publications including Yahoo Finance, Wealth Management magazine, The Detroit News and, as a short-story writer, various literary journals. He is also the creator of the finance newsletter The Root of All (https://rootofall.substack.com/), exploring how money shapes the world around us. Drawing from research and personal experiences, he relates lessons that readers can apply to make more informed financial decisions and live happier lives.

Latest-

My First $1 Million: Banking Executive, 37, Nashville

My First $1 Million: Banking Executive, 37, Nashville

Ever wonder how someone who's made a million dollars or more did it? Kiplinger's My First $1 Million series uncovers the answers.

-

Small Splurges That Won't Derail Your Retirement

Small Splurges That Won't Derail Your Retirement

With decades of growth ahead, your 40s aren't just for saving. We asked financial advisers how to enjoy your income now without compromising your nest egg.

-

How a Tax-Aware Long-Short Strategy Solved This Couple's $50,000 Capital Gains Problem

How a Tax-Aware Long-Short Strategy Solved This Couple's $50,000 Capital Gains Problem

Large unrealized capital gains can create a serious tax headache for retirees with a successful portfolio. A tax-aware long-short strategy can help.

-

5 Retirement Myths to Leave Behind (and How to Start Planning for the Reality)

5 Retirement Myths to Leave Behind (and How to Start Planning for the Reality)

Separating facts from fiction is an important first step toward building a retirement plan that's grounded in reality and not based on incorrect assumptions.

-

I'm a Financial Adviser: Silence Is Golden, But It Hurts Your Heirs More Than You Think

I'm a Financial Adviser: Silence Is Golden, But It Hurts Your Heirs More Than You Think

Talking to heirs about transferring wealth can be overwhelming, but avoiding it now can lead to conflict later. Here's how to start sharing your plans.

-

8 Boring Habits That Will Make You Rich in Retirement

8 Boring Habits That Will Make You Rich in Retirement

These mundane activities won't make you the life of the party, but they will set you up for a rich retirement. Discover the 8 boring habits that build real wealth.

-

QUIZ: Are You Ready To Retire at 55?

QUIZ: Are You Ready To Retire at 55?

Quiz Are you in a good position to retire at 55? Find out with this quick quiz.

-

Will Your Children's Inheritance Set Them Free or Tie Them Up?

Will Your Children's Inheritance Set Them Free or Tie Them Up?

An inheritance can mean extraordinary freedom for your loved ones, but could also cause more harm than good. How can you ensure your family gets it right?

-

I'm a Financial Adviser: This Is the Real Key to Enjoying Retirement With Confidence

I'm a Financial Adviser: This Is the Real Key to Enjoying Retirement With Confidence

A resilient retirement plan is a flexible framework that addresses income, health care, taxes and investments. And that means you should review it regularly.

-

3 Smart Ways to Spend Your Retirement Tax Refund

3 Smart Ways to Spend Your Retirement Tax Refund

Retirement Taxes With the new "senior bonus" hitting bank accounts this tax season, your retirement refund may be higher than usual. Here's how to reinvest those funds for a financially efficient 2026.

-

Trump's New Retirement Plan: What You Need to Know

Trump's New Retirement Plan: What You Need to Know

President Trump's State of the Union address touched upon several topics, including a new retirement plan for Americans. Here's how it might work.